Here's What Cisco Needs to Fix

[Editor’s note: this is an opinionated analysis, based on a wide range of feedback from Cisco customers, employees, and former executives. Cisco does not purchase services from Futuriom and the author has no position in the stock.]

Last week, technologists from around the world attended Cisco Live, the annual conference hosted by the market-share leader in enterprise networking, Cisco. The event was filled with hype and optimism. The irony is there was no acknowledgement of the financial facts of the matter: Cisco’s stagnant revenue growth and stock chart show the company is stuck, while other technology companies vault to new all-time highs.

Let's just put things in perspective: After its last earnings announcement, Cisco shares have fallen nearly 10%. After its AI networking announcements, shares fell again. Cisco's shares are down 10% year-to-date, in the middle of a technology bull market that has Nasdaq at all-time-highs. Cisco hasn't even regained its all-time high from 24 years ago.

More importantly, Cisco is ignoring core weaknesses in its technology portfolio while it's preoccupied by hyping itself In the hottest market—AI infrastructure. The problem is that it's not a leader in the AI networking market, where NVIDIA has the dominant position and hungry public competitors such as Arista Networks, F5, Juniper Networks—as well as startups like Arrcus, DriveNets, and Hedgehog—are building new products.

In 2000, Cisco was considered one of the leading technology companies in the world. Its current market capitalization of $182 billion is still below what it was at the peak in 2000, and it pales in comparison to the multi-trillion-dollar market caps of Microsoft, Google, and NVIDIA, which have exceeded Cisco's value creation by an order of magnitude.

Cisco needs major changes to reverse these trends. Key to its problems are the way it has lashed together hundreds of acquisitions for 20 years or more, yielding little focus or growth.

Fortunately, Cisco is still profitable and has many opportunities, but regaining a growth mindset will require deep cultural and technical changes, based on the feedback we received.

A New Vision Needed

As an analyst, I was eager to see a bold vision about how the company can return to growth and leadership, but the news at Cisco Live was underwhelming. We got the announcement of an AI investment portfolio (too mercenary and superficial), as well as technical integration of Splunk and AppDynamics (compelling, but lacking credibility based on past integrations).

If Cisco really wants to grow its share price, is creating an investment fund to generate investor press releases the answer? Is the company now an investment vehicle? Or does it actually need to sell more products in its core markets?

The conclusion seems to be that yes, Cisco needs major changes. Most of the experts we have talked to over the course of this year have said that Cisco has lost its way. They don’t believe it has a management plan in place to change anything, and they believe it needs to fix its flawed mergers and acquisitions (M&A) strategy. More importantly, it needs cultural change. Cisco executives appear to be in a constant state of hubris and denial—everything is fine! While in discussions in the streets of Silicon Valley, which is filled with ex-Cisco employees, the vibe seems to be that the company has lost its way.

"It's pretty simple, actually—Cisco needs a new, bold vision and mission,” Steve Mullaney, a former Cisco executive as well as the former CEO of networking startups Nicira and Aviatrix told me. “Customers, partners, and employees need this. Why do they exist? Where are they going? How they get there (execution) are tactical details that are relatively easy to do. But they need to know where they are going first and then can get everyone aligned around that vision and mission."

History of Past Glory

Before we suggest changes, let’s cover positives. Cisco is an iconic American technology company that helped create the huge explosion of client-server and business Internet connectivity technology through the 1990s and early 2000s. It rose in the 1990s with the boom in corporate networking, focusing on Internet Protocol (IP) routing and Ethernet technology.

Cisco’s rise in the 1990s was swift and breathtaking, as it quickly gained market share in Ethernet switching and IP routing by buying startup networking companies such as Kalpana and Grand Junction networks to beat out rivals such as Bay Networks. During this period, Cisco rose to become the dominant supplier of enterprise networking technology, and at one time was the most valuable company in the world (with a market capitalization of $500 billion in 2000).

Cisco still makes a lot of money and pays investors a dividend. In reporting its recent third-quarter revenue of $12.7 billion, it had net income of $1.9 billion. It’s a very profitable company and it has a huge installed base.

Cisco's Current Challenges

That’s great. But what now? On to the challenges. Cisco is no longer the dominant force it once was in networking, even though by many estimates it still holds 60%-70% share of the enterprise networking market, but most measures show that it’s losing market share in its legacy markets. Arista Networks' faster growth rate indicates that it continues to take market share from Cisco in core markets such as datacenter switching, and now Arista is ramping up enterprise campus networking.

Most important, Cisco continues to lean on its past glory, and it has not established a path as a leader in any of the new markets it's entered, including cybersecurity, observability, and datacenter networking. Competitors such as Arista Networks have proven they can take share from Cisco with more simple, economical designs. And long-time rival Juniper Networks is a new threat with its forthcoming merger with enterprise technology giant HPE.

The market has shifted. Cloudscale and webscale companies use a different architecture to build networking in the cloud. Many enterprises have chosen to outsource their networking to cloud providers or even network-as-a-service (NaaS) providers rather than build networks themselves.

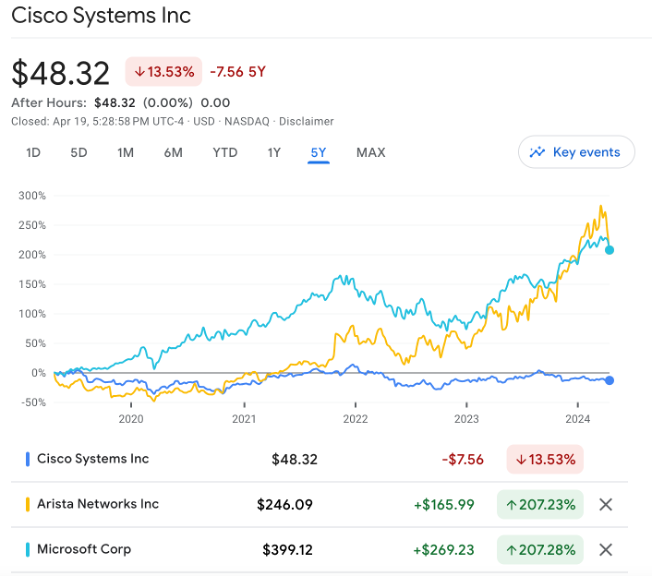

Why is it obvious that Cisco needs fixing? Numbers. The challenges are all reflected in Cisco’s share price, which has essentially gone nowhere in the last five years, during one of the greatest bull markets in history—a bull market that rivals the 1990s, when Cisco rose to dominance.

Cisco’s revenue has been relatively flat over the past five years. From 2019-2022, it hovered in the $50 billion range, as shown in the chart below. Revenue did jump from $51 billion to $57 billion in fiscal year 2023 (Cisco’s fiscal year runs from July to July), but in the second quarter of this fiscal year (2024) it reported revenue of $12.4 billion, down 6% y/y, and projected that revenue for the year will be in the range of $51.5 billion-$52.5 billion, indicating that 2023 was an outlier and that sales will shrink in fiscal year 2024. Going forward, it has guided for about 4%-5% revenue growth.

After last week's analyst day with the financial community at Cisco Live, Cisco gave what was perceived as disappointing guidance, which has weighed on the stock for the past week. In addition, Wall St. analysts have been disappointed (already) by the limited upside from the $28 billion acquisition of Splunk, its largest acquisition in history. Woo Jin Ho, an analyst with Bloomberg Intelligence, wrote in a recent research note that Cisco's presentation last week was disappointing to investors:

"Cisco's fiscal 2026-27 4-6% compounded sales growth view is achievable, but it's down from its prior 5-7% view issued on its 2021 analyst day. The disappointment in the lowered outlook view is compounded by the fact that the Splunk acquisition isn't playing as big a role on top-line growth as hoped. We note the growth from observability and security are expected to be healthy at 15-17%. But networking growth at 2-5% is lagging more than we had anticipated and could be due to some conservatism baked into expectations following several quarters of challenging demand."

Ho also wrote that Cisco could see upside on infrastructure spending in its networking, optics, and silicon businesses, but so far that revenue has not made its way into forecasts.

So far, this continues a pattern of disappointment in emerging technology markets. When you compare Cisco to leading technology companies such as Microsoft, Apple, and Amazon, Cisco’s growth has lagged badly over two decades. Microsoft shares are 40% higher than the peak in 2000, Amazon has grown 3,000%, and Apple has grown an astounding 17,000%. More importantly, those companies all transformed themselves by developing new markets such as cloud infrastructure, smartphones, and AI infrastructure.

In just the past five years, Cisco’s shares have declined 14% while networking rival Arista Networks' shares are up 200% during the same period. Coincidentally, Microsoft shares are also up 200% during the same period.

Source: Google

So, the numbers show that Cisco has a growth problem. The stock chart shows that Cisco has an investor problem.

Fixing the M&A Model

At the core, one of the key problems at Cisco is the company’s core growth model: M&A. This happens frequently in technology, as M&A is nearly always a quick path to organic growth. But Cisco’s M&A history—it's bought literally hundreds of companies—is littered with confusing and perplexing buys. And it’s clear that it hasn’t really delivered much growth, because revenue has been flat for ten years.

One of the common themes of the feedback I got in discussions with sources is that Cisco’s M&A strategy has been underwhelming.

To prove the point: Try to name an acquisition that has made Cisco a leader in a market. Was that Sedona Systems, Portshift, BabbleLabs, or Modcam? Didn’t think so.

ThousandEyes, purchased for $1 billion in 2020, and AppDynamics ($3.7 billion, 2017), are regularly cited as Cisco’s best deals of recent years, but in Cisco’s recent financial statement the network monitoring segment has shown sub-10% growth. Recently, applications and observability leaders such as Datadog and Dynatrace have experienced must faster growth and are considered go-to tools among cloud professionals.

How about some more: Anybody remember Acano ($700 million, 2015); Lancope (“enhances Cisco’s Security Everywhere strategy," $450 million, 2015); Jasper Technologies (IoT, $1.4 billion, 2016); Springpath ($300 million, 2017)? None of these deals has added substantially to Cisco’s growth.

Even somewhat “groundbreaking” purchases such as Viptela (SD-WAN, $600 million, 2017), Duo Security ($2.4 billion, 2018), and ThousandEyes, haven’t moved the needle in a way that was promised.

Cisco’s most sensible acquisition of the past ten years was Acacia Communications, but that was a different genre of acquisition. Cisco bought Acacia for the vertical integration of a component supplier—a financial engineering play. Acacia was a large provider of Cisco optics, so buying a supplier meant that Cisco could boost margins and pursue more vertical integration in its systems while controlling supply. In this sense, it worked out well.

The jury is still out on Cisco’s largest deal ever—the $28 billion acquisition of data analytics provider Splunk, which only recently closed. So far, this looks like a revenue grab to reorient Cisco’s revenue toward software. But as a data observability and security company, Splunk has some overlap with AppDynamics and ThousandEyes. In order to do the deal correctly, Cisco will have to integrate the portfolio in a sensible way that doesn't alienate customers.

Ho sums up the problem well here in a research note:

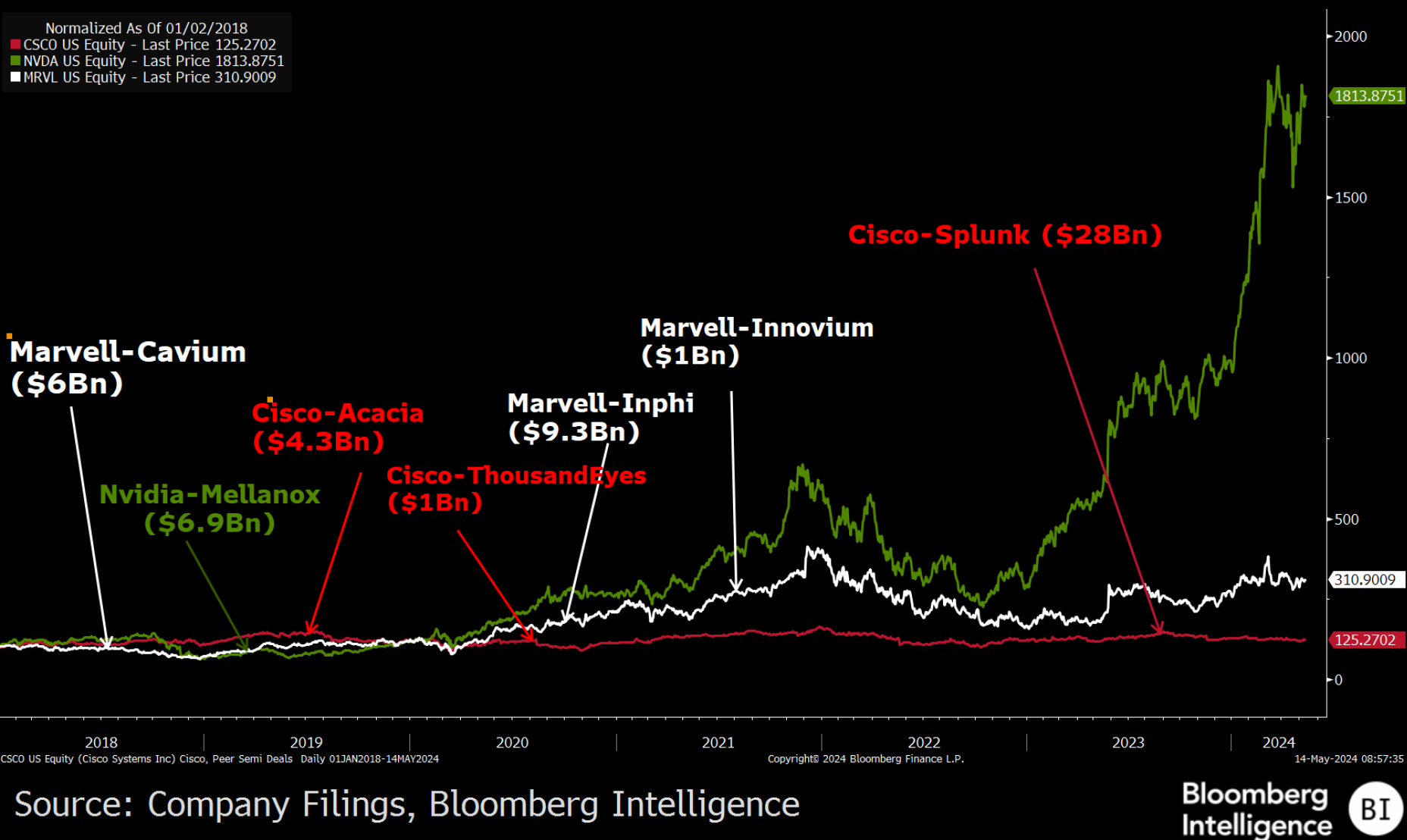

"Cisco's ability to navigate around the "Innovator's Dilemma" is a real challenge given its market leadership across key markets. Since Chuck Robbins took over as CEO in 2015, deals have embraced the need to add next-generation technologies to limit disruptions. Insieme (softwaredefined networking), Viptela (software-defined wide-area networks) and Acacia (high-speed optics) addressed key trends such as network virtualization and convergence. But its focus on transforming its business model may have resulted in missed opportunities in making transformative high-growth semiconductor deals, such as Mellanox (AI networks) and Cavium (data center chips). Its Luxtera and Acacia deals appears to acknowledge the strategic value of chips, and we think a more assertive effort in this area could have changed its growth

narrative. (05/13/24)"

The chart below, used with permission from Bloomberg Intelligence, shows how infrastructure rivals such as Marvell and NVIDIA have seen more success from their strategic acquisitions. NVIDIA's acquisition of Mellanox, which is now a key networking technology in its AI infrastructure, might be deemed as one of the most successful deals of all time.

Another reason why Cisco may lack credibility with the Splunk deal is because it has a proven pattern of leaving acquired products as islands in the portfolio, such as Meraki. Cisco bought Meraki in 2012, but it’s still a standalone product line.

“[I]t has been a predictable cycle of buying revenue streams or bandaids for existing businesses and then laying off staff to reach profit targets,” one former Cisco employee wrote. “I've been gone since 2011 and it has been many years since I've heard any employee talk passionately about the company or show the spirit and drive that was so pervasive when I joined. It's sad.”

Networking and Operating Systems Need Fixing

As Meraki demonstrates, one of the flaws in Cisco’s M&A strategy is a lack of integration. This has generated significant ill-will from Cisco’s user community. Big product lines, such as Meraki, maintain different network operating systems (NOSs) and management systems. This serves as a hindrance to users rather than a benefit, as they need to toggle among management screens for different pieces of the portfolio.

Cisco IOS, Cisco IOS XE, Cisco IOS XR, Cisco NX-OS. Take your pick. But that's not all, there are also many other operating systems and software products often required to build the same network. There's Application Centric Infrastructure (ACI) and DNA. Cisco Meraki. Dive into any Cisco technical forum and you will find people confused and frustrated by the separate portfolios, as well as strange situations in which Cisco products compete with one another.

Cisco has dozens of operating systems layered on top of one another. And then there are licenses. When we talk to end users, one of the top complaints about Cisco is that licensing is very complicated. Customers can spend more time managing the networking licenses than the actual technology, a fact that Cisco competitors such as Extreme Networks have taken advantage of by offering a "one license" plan.

“The meta challenge for Cisco is 10s of versions of software and no single OS,” a prominent Silicon Valley investor, board member, and former Cisco executive told me under condition of anonymity. “Also, topped by poor business decisions and lack of strong technical leadership mean no one even understands the problem they have.”

“Cisco cannot be fixed until it fixes its networking business,” the former Cisco executive told me. “That business is losing share much faster than people realize and is covering it up with three-year license deals to software. When those deals expire, customers churn. So what they have is a dying installed base, tired of overpriced and poor tech.”

Crowdsourcing the Cisco Fixes

So what should Cisco do? The feedback from our sources indicates there is continued uncertainty about Cisco’s direction, leadership, and investors connected to Cisco.

Many of our sources are past and/or current employees or customers of Cisco. For this analysis, we decided to reach out to the market to see what people said. Here’s the bottom line of our assessment, based on our conversations with dozens of people: Big changes are needed to right the Cisco ship, which is adrift in a sea of mediocrity. Here are some of the key points:

Reduce the NOSs and licenses. Customers are overwhelmed by code and license management. They want a more streamlined Cisco portfolio, with easier-to-understand licensing. Cisco has not done a great job of integrating networking products, and it should start by consolidating the numerous NOSs.

Reduce the number of products! The number-one complaint among Cisco users is that they are pummeled by the sales force to buy more products. Provide more value, rather than selling everything. A common customer complaint is “They sell us too many products, we’d rather they provided more value.” Customers feel like they are being used by Cisco rather than provided better service.

Combine Splunk, AppDynamics, and ThousandEyes. Is Cisco’s objective just to buy a software company, or do they want to be the leader? Splunk, AppDynamics, and ThousandEyes are all standalone observability and data products that have their own applications and data lakes. At Cisco Live, Cisco took the first steps to integrate Splunk and AppDynamics, but the long-term strategy to unify data from all these product lines to improve automation and security is still unclear. But if Splunk is “Meraki’d” and left as an island, it will be a disaster, because companies such as Datadog and Dynatrace will eat their lunch.

Be more humble. Cisco’s marketing and sales culture is over the top. Every vendor uses too much jargon and marketing nonsense, but Cisco’s marketing is more jargonated than most and is hard to understand. In my experience, the company culture is overly concerned with celebrating itself, instead of looking in the mirror. It's stagnant $190 billion market cap, which has not budged in decades, shows the result of this.

I would ask Cisco executives whether they are just thinking about paying dividends and stock buybacks, or if they are actually worried about long-term innovation and potential failure. Jensen Huang, the CEO of NVIDIA, has said that he regularly wakes up from sleep thinking about failure.

Some might argue that Cisco doesn’t need to be fixed, but the evidence and feedback I gathered points that it does. The share price says everything: Investors are frustrated, not rewarded. With competition growing faster than ever, Cisco needs to fix things rapidly or investors might be left with another decade of dead money.