Can Media Save Telecom?

AT&T (T) has bet the farm again, this time with an $85 billion merger with Time Warner (TWX). After a challenge from the U.S. Justice department, a judge has finally approved the deal. This follows another enormous $49 billion deal for DirectTV in 2014.

This is a high-profile business experiment that combines one of the world's largest telecommunications firms with one of the world's largest media companies. And it's a huge gamble because of the massive amounts of debt that AT&T has accumulated.

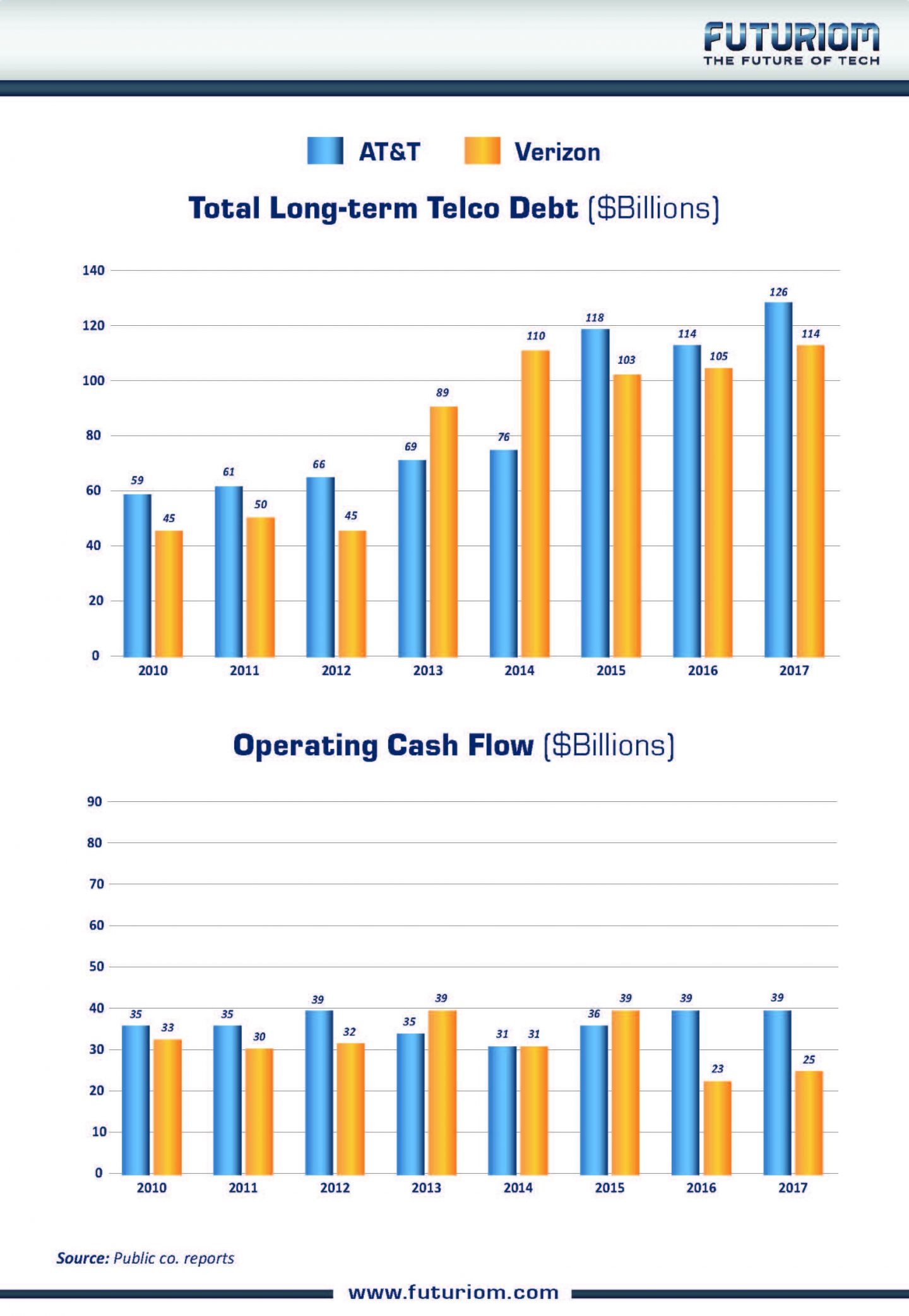

Over the years, the two North American giants, AT&T and Verizon (VZ), have massively increased their debt to pay for acquisitions, capital investment, and spectrum licenses.

AT&T's Debt has climbed from $59 Billion in 2010 to $126 billion at the end of 2017 -- growth of more than 100% in less than a decade. Verizon's long-term debt has increased from $45 billion to $114 billion since 2010 -- growth of 150 percent. During the same period that their long-term debt has doubled in scale, the operating cash flows of these companies have barely budged. AT&T's annual cash flows have gone from $35 billion in the period to $39 billion. Verizon's have actually declined -- from $33 billion in 2010 to $25 billion in 2017. (All numbers taken from public annual reports.)

I have written a more detailed analysis of this issue over on Light Reading. But here's the Cliff's Notes version: As the charts below show -- each of these giant telcos has increased their leverage while operating cash flows have remained flat. As anybody with a growing mortgage and flat salary would tell you, that's not a good formula.

Why such a leveraged expansion? The telcos are trying to diversify into content. So far, there is little evidence it will work. AT&T's DirectTV unit lost more than 1 million paying customers in 2017.

Then there's the competition. Over the years, more data-savvy Internet companies such as Amazon (AMZN) and Netflix (NFLX) have shown they have better capabilities to service consumers and monetize content.

Investors and business partners need to track these debt levels closely because with interest rates rising, they become very dangerous. For ever one percent rise in interest rates, AT&T and Verizon's annual debt payments are likely to rise by $1 billion (each) or more. They need to prove very quickly that they can take these new media assets and use them to generate more profitability. Otherwise there could be big trouble ahead, including a private debt crisis.