Can IBM Be Saved?

IBM shares plummeted more than 25% this week on news that IBM infrastructure hardware and software failed to sell to customers who instead chose to focus on AI requirements in the face of supply-chain shortages.

It’s the biggest selloff in recent IBM history, and the largest since January 3, 1968, according to Bloomberg.

So what exactly went wrong? And is IBM going down a slippery slope, or can its selloff be reversed? Let’s take a closer look.

Sad Numbers

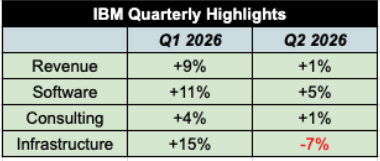

To start with, the figures: For IBM’s Q2 2026 (to be announced July 22), quarterly revenue of $17.2 billion is up just 1% and lower than analyst projections of $17.9 billion. Adjusted EPS will be $2.93, below analyst consensus of $3.02.

For IBM’s Q1 2026, revenue was $15.9 billion, up 9%; analyst consensus was $15.7 billion. Adjusted EPS was $1.91; the Street projected $1.81.

The trouble lurks in the segment numbers: Last quarter, software was up 11%; this quarter, it’s up 5%. Last quarter, consulting was up 4%; this quarter, it’s flat. And most telling, last quarter, infrastructure, including IBM’s new z17 mainframes, was up 15%; this quarter, it’s down 7%.

Digging Deeper

Surely, IBM is suffering from a range of industry trends. In a letter to investors this week, IBM CEO Arvind Krishna stated that IT customers have “reprioritized” their capital spending for at least three reasons:

- First, prices are going up as a result of AI. As producers of memory products such as SK Hynix, Samsung, and Micron juggle their production between high-bandwidth memory (HBM) needed for AI and products to meet consumer demand, supplies are shortening and prices increasing.

- Second, supply shortfalls have organizations scrambling to get hold of storage, server, and memory products. Apparently, IBM didn’t bank on this trend and focused instead on mainframe-based deals, which failed to materialize as planned.

- Third, cybersecurity problems raised by Anthropic’s Claude Mythos model and other sources have customers worried about products highlighted in the quarter, and IBM’s are no exception.

The above causes cited by CEO Krishna prompt questions about why IBM suffered so much from the trends. If customers are looking at storage, server, and memory products, why not turn to Big Blue, which has all those things?

The answer seems to lie in IBM’s priorities. This quarter, its ongoing rollout of the z17 mainframe, touted by IBM for its AI capabilities, failed to grab the revenue IBM had hoped it would. Even allowing for a lag as sales ramped, the z17 and its associated software, especially for transaction processing, were a dud.

Failure to Launch z17

There are a few possible reasons for IBM’s failure to launch its z17 effectively. Customers don’t want mainframes; they want accelerated compute pods powered by NVIDIA GPUs. Competing with that architecture isn’t serving IBM well, though IBM has worked hard to bring AI capabilities to its hardware and software infrastructure, increasing the AI capabilities of its mainframes as well as of age-old software favorites such as Db2 and Cognos.

IBM's investment in the mainframe was reflected in remarks by IBM CFO James Kavanaugh on the company's earnings call last April:

“[M]ainframe modernization increases the strategic importance of IBM z.... Why? Because the source of value is architectural. It's the platform. It's not the language. It's a tight integration of software, hardware, database, security, run time, resiliency…. [T]his is a whole new monetization area of opportunity for us on that platform stack.”

Customers are turning away from IBM's mainframe-based stack in favor of software powered by models from OpenAI, Anthropic, and leading hyperscalers, which also offer their own services for AI processing. The popularity of those services, and the astounding growth of neocloud and altcloud services, prove that enterprise customers want GPU-based AI factories, not mainframes.

The growing popularity of open-source AI software is another force threatening IBM. As the Wall Street Journal put it, "The SaaS-pocalypse has come for IBM." Futuriom's research also shows that proprietary AI models derived from a range of sources represent the foundation for a majority of enterprise AI applications.

The Good News

IBM still has plenty to offer. Its Power servers and storage products, including NVIDIA-compatible storage solutions, realized 37% growth in the quarter, Krishna stated in his letter. There is also a backlog of $500 million for those offerings exiting the quarter, he said.

IBM and Red Hat in May also formed Lightwell, a division created to help enterprises secure open-source software. With $5 billion in financing and a dedicated army of 20,000 engineers, the effort is designed to be, according to the press release, “a trusted enterprise clearinghouse combined with a global force of engineers to identify and fix vulnerabilities at scale.” The effort feeds into a clear industry need and leverages IBM's strength as an IT infrastructure supplier.

IBM is also relying heavily on its future in quantum computing. Having created a quantum chip foundry and associated R&D support, IBM remains “on track to deliver the first large-scale fault-tolerant quantum computer by 2029,” Krishna wrote. Though the future of quantum isn't yet clear, IBM is betting heavily on succeeding in that market.

Futuriom Take: IBM needs to rejigger its priorities to focus more on its strengths, including distributed computing with AI support and cybersecurity. Arvind Krishna’s efforts to turn the ship around have helped, but more is needed if IBM is to get on board with key AI trends.