Arista Shares Hit All-Time High

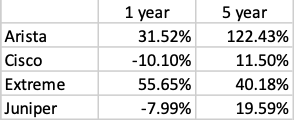

Arista Networks (NYSE: ANET) is riding high. Over the past month, the switching vendor’s share price has risen over 15%. And that’s not only a result of its stellar fourth-quarter earnings report on February 13. Over the past year, Arista’s stock has grown more than 31%. Over the past five years, it’s grown over 122% in value. This week, shares hit an all-time high: As of this writing, they were trading at $163.93, up 10.08 (6.59%).

To put things in perspective, Arista appears to be enjoying a general upswing in demand for datacenter switching and routing. Rivals Juniper Networks (NYSE: JNPR), Extreme Networks (Nasdaq: EXTR), and Cisco (Nasdaq: CSCO) also saw shares rise recently, thanks to growing demand from cloud providers, telcos, and enterprises. But so far, only Extreme has shown growth that rivals Arista’s, albeit at a much lower share price, as shown in the table of share price growth below:

Source: Google Finance

What’s Arista’s secret? There appears to be more than one. Let’s take a look.

Arista Sees Ahead

Arista’s good at reading the tea leaves. Two years ago, management saw the opportunity in campus switching with emphasis on a secure edge. A year later, Arista predicted it would reach $400 million in campus switching in 2022 – a goal it reached despite supply chain shortages. Now Arista’s goal is to reach $725 million in campus revenue by 2025.

Arista foresaw the market for 400-Gbit/s Ethernet datacenter switching and has succeeded in producing 800-Gbit/s systems interoperable with its 400-Gbit/s connections. The company also spied an opportunity to cut into the market for InfiniBand in high-performance computing (HPC) “[W]e have an opportunity to replace InfiniBand,” said CEO Jayshree Ullal on last month’s earnings call.

Now Arista has its eye on artificial intelligence (AI). Specifically, the vendor sees enormous opportunity in providing the high-speed Ethernet network for emerging AI workloads. By multiplying the amount of bandwidth between AI clusters, Arista can serve the growing market for AI applications. Here’s how CEO Ullal put it in a recent blog:

“A typical structure of an AI workload involves a large sparse matrix computation, so large that the parameters of the matrix are distributed across hundreds or thousands of processors…. A modern, scalable AI network is imperative….

"In the past, this sort of performance existed only in the domain of specialized HPC networks such as InfiniBand. Today the combination of RDMA Ethernet NICs and RoCE (RDMA over converged Ethernet) allows Ethernet and IP to be used as the transport fabric without overhead.”

From Products to Platforms

Arista has moved from strength to strength in part because of a cohesive product strategy. Recently, that strategy has focused on offering platforms, not individual products. “2023 is the start of Arista's 2.0 journey. Arista 2.0 is our migration from best-of-breed products to best-of-breed platforms,” said CEO Ullal on the latest earnings call.

A basic element of this platform approach is Arista’s common underlying Extensible Operating System (EOS). “We aren’t bolt-on,” said Martin Hull, Arista VP, systems engineering and platforms, at a recent investor event. “I think we are alone in the industry at this point in time in having a pure operating system software code.”

That software is a key element of the datacenter switches, including the flagship 7800 Series, that Arista sells to hyperscaler cloud providers. “[O]ur core cloud and data center products [are] built upon a highly differentiated Arista EOS stack that is successfully deployed across 10, 25, 100, 200, 400-gig speeds. This drove approximately 68% of our revenue with strong cloud and enterprise spending cycles,” said CEO Ullal on the recent earnings call.

Arista’s "M&M" Exposure

If there is a cloud on Arista’s rosy horizon (pun intended), it may be its reliance on two of the world’s biggest datacenter customers – Meta Platforms (Nasdaq: META) and Microsoft (Nasdaq: MSFT). Of Arista’s $4 billion in sales for fiscal 2022 (up 48.6% year-over-year), 25.5% were from Meta and 16% from Microsoft. The rest of Arista’s 9,000 customers include engagements with at least two of the other top hyperscalers, along with enterprises and service providers.

But clearly, Arista is heavily exposed to “M & M." Given that Meta is on a slim-down plan, could that be risky? Not a problem, management says. The cloud titans continue to expand their facilities and Arista continues to supply them. “We remain confident about meaningful share with both Microsoft and Meta, and we expect both of them to once again contribute greater than 10% of our total revenue in 2023,” said Ullal on the earnings call.

Bottom line? Arista appears to be a key contributor to the cloud market for the foreseeable future, and its prescient market moves make it a bellwether for cloud infrastructure trends.