What Does the Banking Crisis Mean for Cloud Tech?

What does the banking crisis mean for the cloud? This might be hard to believe, but so far the market is signaling that it’s good.

How could that be, you ask? Silicon Valley’s eponymous and iconic bank, SVB Financial, has failed and filed for bankruptcy. An iconic Swiss bank, Credit Suisse, had to be rescued in a partnership between the Swiss National Bank and UBS. A number of other regional banks in the U.S. appear to be on the ropes. Federal banking officials are scrambling to contain the damage.

But technology and cloud stocks have been rallying lately. In the past week, Amazon shares are up about 7%, Microsoft has rallied about 8%, Google is up 10%, and Apple is up 7%. Some brand-name chip companies are still riding the artificial intelligence boom, despite the banking crisis. Shares of NVIDIA are up 77% year-to-date (ytd), for example. And Arista Networks, as we pointed out last week, recently hit an all-time high -- attributable partially to cloud gains as well as its potential for networking AI applications.

Recently, large tech companies such as Amazon, Facebook, and Microsoft have also been trimming expenses and announcing reorganizations in the face of slowing growth, indicating to investors that they will be watching costs, which typically pleases investors (but not those that have been laid off). This could further boost profitability in the future.

So what's going on? A lot of it might have to do with the direction of interest rates. Let's walk through all the details.

Cloud Tech Is Stable and Cash Rich

The first explanation for the health of the cloud tech sector just comes down to money. The current banking crisis is concentrated in a few banks that had to take losses on treasury portfolios, which suffered as they stuffed their balance sheets with deposits when interest rates were low but then suffered losses as interest rates spiked.

Most of the largest and cash-rich tech companies have rock-solid balance sheets with large amounts of cash, so unlike many enterprises, they aren't over-leveraged in debt and can be a port in the storm. For example, at last count, Microsoft had an astounding $103 billion in cash and short-term investments. The largest tech companies are also massively profitable. Microsoft made $72 billion in profit in 2022, and Google made $60 billion in profit. They are in absolutely no danger.

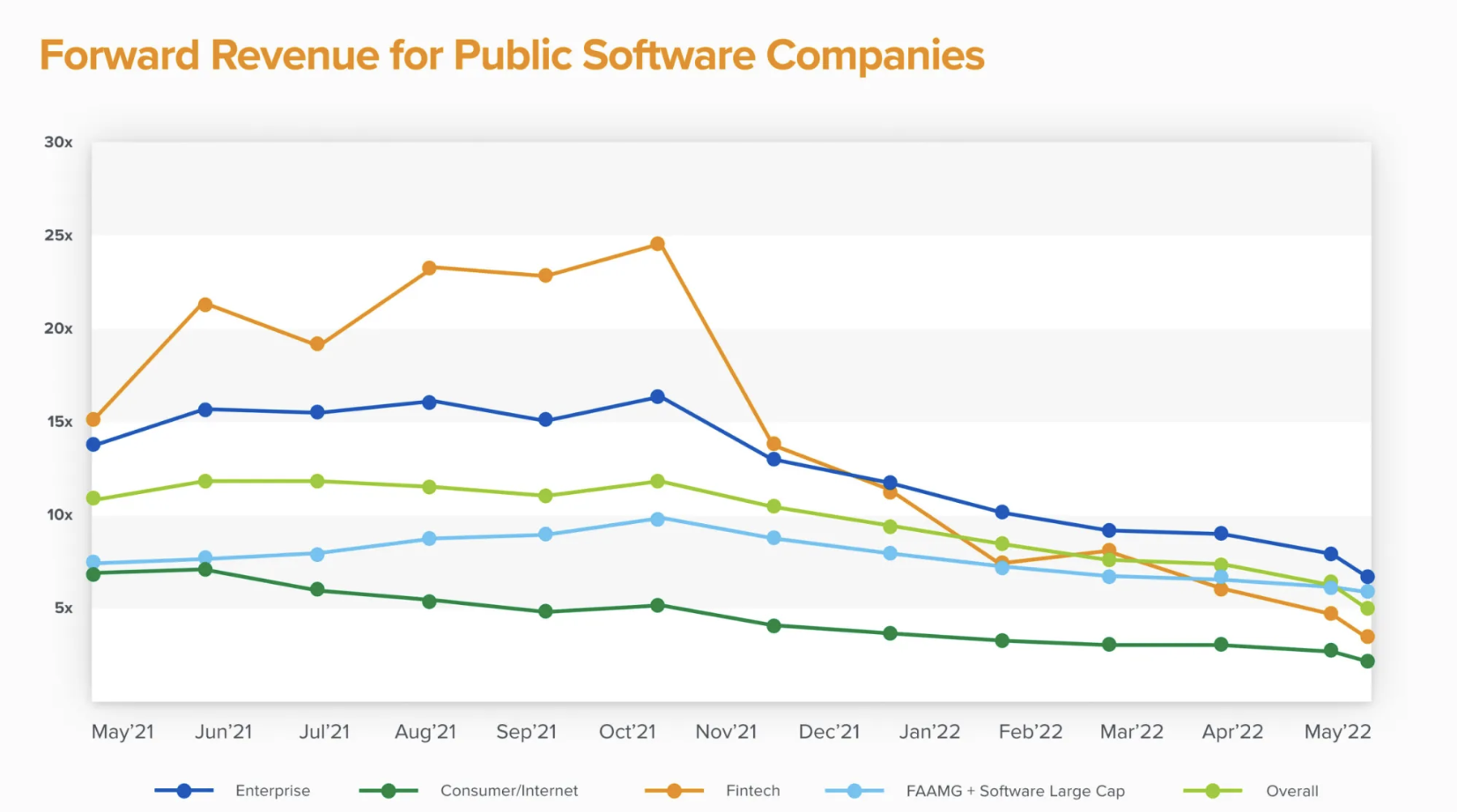

The main reasons that technology stocks went down last year is "multiple compression," or their valuation based on a multiple of price/earnings ratio. Technology growth companies typically have valuation multiples that are inversely correlated to interest rates. Because they are priced on future profits, the valuation multiples compress as interest rates rise -- which was the primary driver of valuation compression across the technology segment in 2023.

The chart below, from Andreessen Horowitz, shows you what happened to tech valuations in 2022 as interest rates were hiked:

Source: Andreessen Horowitz

Interest Rate Trend Is Good for Tech

Market-based interest rates have stabilized and in fact dropped in 2023, leading to a tech rally. A sensible way to view it is that technology valuations skyrocketed in the 0% interest-rate environment, but now they have largely normalized. So any drop in interest rates will be good for tech in the long term, as a dropping cost of capital will stimulate investment.

The U.S. Federal Reserve meeting is tomorrow. The recent banking crisis has lowered the market expectations of future interest rate hikes, so it is expected that they may temper their view. Nearly everybody expects them to signal some kind of slowdown or pause in the rate hikes, which have triggered the current banking crisis. The way the market reacts to any moves will be crucial. Of course, if they stay the course for rates above 5%, the market may not like that.

Another factor: The growing risk of recession, along with a softening job and house market, means that inflation is likely to continue subsiding (the Fed did exactly what it wanted to do, which was stop the economy and stock market in its tracks).

What Caused the Boom/Bust Cycle?

To me, it seems like there has been too much analysis of the current banking crisis, Silicon Valley Bank, and other current factors -- rather than a simple acknowledgement of the remarkable boom-bust economy created by the huge financial response to COVID and how it fueled the economy, including the banking and technology sectors.

Money's got to go somewhere. The tech markets were a major beneficiary. Trillions of dollars flowed into consumer pockets and banks as the world retreated into their homes for hybrid work and endless video streaming. These trends caused cloud infrastructure and related services to boom.

All this money contributed to inflation. As inflation started rising in 2021, global central banks were generally slow to respond -- waiting for inflation to crack 4% before they started hiking. Then the hikes came fast and furious. Last year, the Fed raised rates at a historic rate while withdrawing liquidity through a reverse of the process known as Quantitative Easing (QE), which is now known as Quantitative Tightening (QT).

This combined with a unique change in the economy -- lockdowns ended, people returned to the office, supply-chain challenges eased, and the Fed withdrew liquidity. Some sort of chaos was inevitable. The largest technology companies in the world pulled back. They started cutting investments and laid off large numbers of staff – most of them hired during the COVID period to fuel the COVID cloud services boom.

The banks, meanwhile, had to soak up all that extra COVID money in the form of booming deposits, and some of them did a miserable job of managing those deposits.

So, you see – it’s all related: Gigantic COVID stimulus > money bubble > huge cloud investment > inflation > yield spike > bank losses.

So, what’s next, you ask?

It’s Not that Bad

First of all: Calm down, it may not be that bad. At least not as bad as 2008.

So far, the losses pale in comparison. Lehman Brothers had $800 billion in assets when it failed. SVB had less than $200 billion and Credit Suisse had about $500 billion. Many of the assets in the banks are in safe holdings such as government bonds, and governments have largely guaranteed much of the deposits so the losses don't look nearly as big. So far, we haven't had a Lehman moment.

The next question you might have to ask is: How will the problem be solved? The solution is rather simple. The crisis was created by rising interest rates, which caused losses on government bonds bought at very low yields. So, all you have to do is lower interest rates to reverse the pressure – and in fact reverse the losses, as they were primarily caused by losses on bonds.

This is already happening in market-based mechanisms, as I mentioned. The 10-year treasury rate has been falling rapidly, as has the two-year yield. That means the prices of government bonds have already risen substantially, alleviating some of the pressure. It looks as if it’s going to become harder and harder for the Fed and other central banks to justify raising rates and holding them higher.

No doubt, it's been a chaotic period. But what to expect? There has never before been anything like COVID, or the trillions of dollars of money thrown at it. The technology investment bubble created by this influx of cash has subsided. Now interest rates are subsiding as well.

In short, it looks like we are going through a difficult period as we try to return to normal. As interest rates stabilize, inflation cools, and the economy slows down, it will be easier for markets to regain a sense of normalcy.

In the long term, with AI and other digital services surging, does anybody expect the cloud to go away? One might take the view that cloud tech is now healthier than ever -- investment has been right-sized, valuations are closer to rational, and cloud services and technology are still producing growth. It's going to continue to be one of the most attractive sectors in the economy.