A Deep Dive Into Cisco's Growth Challenges

Who's up for a deep dive on trends in Cisco's business and earnings? My quarterly review of Cisco's earnings was delayed due to the release of our SD-WAN Growth Report. Last week, Cisco (CSCO) reported its fiscal fourth quarter earnings and the headlines blared, with conflicting views from both journalists and analysts.

The bottom line? Cisco just isn't growing. I'll detail why not and why that's unlikely to change anytime soon. But first, more of a review of what was said.

There was stuff like this:

"Cisco's revenue has declined for 7 quarters — but the signs of a comeback are already visible," shouted Business Insider.

"Cisco Slides After Revenue Beat," stated CNBC.

But here's my favorite: "Cisco Systems, Inc. (CSCO) Stock Dips on Toothless Q4 Earnings."

Toothless! Seems a little harsh. I mean, after all, they make money -- so the earnings had teeth.

Having covered technology earnings for 25 years, I am always fascinated by the variety of reactions and interpretations you can see from the same numbers.

The bottom line is that there has been little change in trend from the numbers in the earnings report during the last year. Cisco's revenue still shrinking, security revenues were disappointing, and perennial challenging areas such as service provider market look... well, perenially challenging. But the company is still bringing in cashflow at a regular clip at about $2 billion a quarter. In 2017 it banked $11.7 billion in cash, up from $7.6 billion in 2016. That's built up a nice war chest of about $70 billion in cash and investments on the balance sheet.

Cisco executives are doing their best to put on their game face and talking about a multi-year project to transform the company to more of a recurring software subscription revenue, but that transition appears to be happening very slowly -- and not without risks. Some Wall Street analysts are buying into this story, pointing to the growth in Cisco's deferred product revenue, which is an indicator of their transition to subscription packages generating recurring revenue, rather than equipment sales.

As George Notter of Jefferies put it in an investment note last week:

"Recurring revenue now accounts for 31% of company sales, up from 27% a year-ago (these are the same metrics they referenced a quarter ago). They continue to push customers toward the CiscoOne subscription model – they now have 20,000 CiscoOne customers, up versus the 18,000 they disclosed at the Analyst Day."

It's great that Cisco's focused on recurring revenue. But is it happening fast enough? The overall numbers indicate that is not the case. Most of Cisco's product areas are shrinking. For example, take a look at the year-over-year product group numbers for Cisco's fiscal year, ending July 31:

| Category | Revenue | Percent Change |

|---|---|---|

| Switching | $14 billion | (5) |

| NGN Routing | $7.8 billion | (4) |

| Collaboration | $1 billion | (4) |

| Data Center | 767 million | (5) |

| Wireless | $703 million | 13 |

| Security | $527 million | 9 |

| SP Video | $207 million | (30) |

As you can see, Cisco is only growing in 2 out of 7 categories! And Cisco's largest revenue areas are struggling the most -- with little end in site for relief for routing or switching, unless you expect the enterprise switching or service-provider routing market to come roaring back anytime soon.

Tough Trends for Cisco

Part of Cisco's growth challenge is being a large company -- moving the needle on $50 billion in revenue is not easy.

But there are also larger industry trends that are slowly growing and challenging Cisco. Here they are:

1) Enterprise Has Moved to the Cloud

Cisco grew up with rocket-like growth in the mid-1990s, when local-area networks (LANs) were the rage and every company and branch office needed Ethernet switches the way households need TVs.

But now those enterprise Ethernet switches and routers have been commoditized. Cheap commodity off-the-shelf (COTS) chips mean that Ethernet switches are available everywhere, and they're basically like... well, televisions -- hard to differentiate. Meanwhile, the bulk of IT hardware growth has moved to the cloud and "webscale" players, who are doing some unique things, and in many cases they are building their own switching infrastructure.

Google, for example, builds its own switches. Facebook introduced the "Wedge" switch, based on COTS hardware. Both companies -- and many others including Amazon -- are building their own sophisticated routing software. They really have no need for many of Cisco's products -- especially not its software, which is not regarded as cutting-edge in the industry.

Of course, that doesn't mean Cisco doesn't sell into cloud -- it does -- but it has a relatively small share. When you stack up Cisco against other hardware vendors selling full cloud switching solutions, such as Arista, Cisco is not growing as fast -- meaning its share is stagnant to shrinking. So it's hard to be optimistic here.

Research firm estimates that Arista is gaining share from Cisco in the important datacenter switching category for 100-gig ports. Arista has gone from single-digit share to nearly 15 percent share of the market for high-speed data ports.

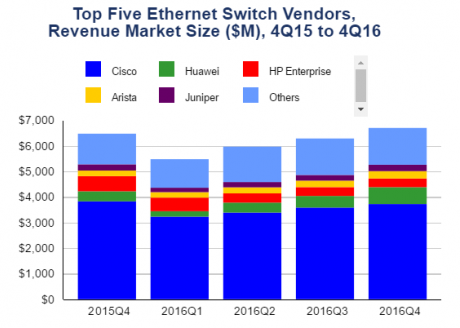

But that's not all. Cisco is being squeezed from both sides because Chinese technology conglomerate Huawei, which is even bigger than Cisco ($80 billion versus $50 billion in revenue), is also taking share from Cisco. See the chart below.

2) The Telecom Market Sucks

I've always wondered whether Cisco executives secretly hate the service provider market. They would have good reason for this. Look at what the service-provider market did to Nortel Networks (now deceased), Alcatel-Lucent (now part of Nokia), and Ericsson. The surviving companies have been forced to merge in the face of a shrinking market, with the remnants of Lucent and Alcatel now couched like Russian nesting dolls inside Nokia. All these remaining players duke out for large, ultra-competitive contracts with intense margin pressure. It's not a fun business.

Let me just give you an exmaple: Nokia's gross margins from the most recent quarter are 40 percent. Ericsson's gross margins are 28 percent. Cisco, in comparison, has a relatively attractive gross margin of 60 percent, so the service-provider business, which has been cited as a problem in recent quarters, is dragging down margins.

It may get worse. Not only are the dynamics of the service provider business bad -- with the software value of connected devices and cloud software accruing to other players such as Apple and Amazon -- but the service providers are trying to act more like cloud providers themselves, which means they want to build their own networking infrastructure. Talk about nightmares for hardware companaies.

Just as Cisco may secretly hate service providers, service providers often secretly whisper their distaste for Cisco, in private conversations. They don't want to be chained to an expensive, single-vendor solution that locks them into services contracts. Why not try to be more like Google, and buy cheap parts that you can glue together with open-source code?

It sounds great on paper, and large service providers such as AT&T have publicly announced a move in this direction. Whether it will succeed is another story, but the long-term impact is not good for Cisco or other service-provider routing and switching vendors such as Juniper Networks.

3) Cisco's Security Strategy Isn't Growing Fast Enough

Cybersecurity. Heard of it? It's in the headlines every day. In many markets, Cisco actually has majority of market share. But in the most recent quarter, its security revenue only grew by 3 percent!

Palo Alto Networks (PANW) has $1.6 billion in revenue and year-over-year growth of 25 percent. Basically, little PANW is almost as big as Cisco's security business, and it's growing faster. Other startups are picking up large chunks of the security market as well -- for example, FireEye (FEYE) has about $800 million in annual revenue. IBM doesn't break out specific security revenues, but many analysts estimate that at about $2.1 billion. IBM said in public reports that the security business grew 7 percent in 2016.

4) R&D Spending Is Flat-to-Down

So where are the changes going to come from? Recently Cisco has been touting the "biggest innovation in a decade" with its intuitive networking initiative. As I have detailed before, so far this is mostly marketing rhetoric with technical details hard to come by.

Where does innovation come from? It comes from either research and development (R&D) spending, or from acquisitions. Traditionally, Cisco has relied more on acquisitions. In fact, recently its R&D budget has been shrinking, going from $1.6 billion in the quarter a year ago to $1.5 billion in the most recent quarter.

Conclusion: Difficult Path Forward

To summarize, there is a ton of competition for Cisco in nearly all of its core areas. In enterprise switching, it's getting cannibalized by COTs hardware and low-cost players such as Huawei. In datacenter switching, it's being squeezed by Arista and Huawei. In security, it has to contend with a raft of startups as well as other giants such as Checkpoint and IBM. Routing is not as important a market as it used to be, as many routing functions have been subsumed by all-purpose Ethernet switching.

While the shift to a recurring software model is a nice thought, there's no sign of this moving the needle yet. There's also no indication that Cisco has a competitive edge here, other than its gigantic sales force. Cisco's biggest subscription offering, the Cisco ONE software platform, offers security and analytics tools -- many of which are available from competitive players.

Cisco is also reducing its R&D spending. Cisco is not known for internal product development, so the way forward will be for Cisco to continue to make acquisitions such as the recent AppDynamics. The most attractive part of AppDynamics is its software model. One venture capitalist, Tomasz Tunguz, has some analysis that shows Cisco may have paid the biggest M&A multiple in history, on the basis of enterprise value/revenue. Cisco's deal for Viptela, at $610 million, was also not cheap, coming at an estimate multiple of at least 10X revenues, though Viptela's revenues have not been disclosed.

To get to where it wants to go -- grow software revenue -- the company will have to continue to snap up companies. Expect Cisco to keep hunting for software revenue to grow its software business. This strategy will not come cheaply.